Question 13: With the move toward greater utilization of “opportunity crudes” such as Canadian synthetic crudes, what shifts do you expect in FCC product yield and quality, and how will this impact the operation of the FCC unit?

HOWELL (Holly Refining)

Holly’s choice for opportunity crudes are somewhat limited by our position as an inland refiner and being located far away from many of the crude pipelines. We are making changes in both the way we operate our units, as well as our capital investment, so that we can maintain our current slate with crudes of varying quality. With the opportunity crudes that we do run, we have already experienced increased levels of traditional FCC catalyst poison. Our response to that has been increased catalyst makeup, evaluation of additives, and consideration of custom catalyst blends. We are adding mild hydrocrackers at both refineries and we expect to see a large change in our heat balance. If our crude sources change to include previously upgraded stock or crude blends, then we would expect to see our coke yield and heat balance put back in the direction of where we are today.

As in the rest of the industry, our ultimate goal is to maintain quality products and maximize yields from feedstock survey that will come with discounted and benchmarked crudes. We will continue down this path of making capital investments, catalyst changes, and additive use to try to do that. The bottom line is that we have not yet experienced anything other than that buildup of what we consider to be traditional FCC catalyst poisons. So, expect to see some changes in the very near future.

HEATER (BASF Catalysts)

All syncrudes will be processed by cokers and hydrotreaters ahead of the FCC so there is no single, generic answer. The key will be to crack the fully- and partially-saturated ring structures. With syncrudes, FCC feeds will tend to be less paraffinic and more aromatic with resulting lower conversion. Depending on the degree of hydrotreating, lower gasoline yields will be seen but will have higher octane and benzene content. You will see a higher LCO yield with the lower cetane. You will tend to see higher decant yield with lower API gravity so there is a potential for some fouling issues. BASF is developing catalysts in this area and we will be coming out with something in the very near future. In the Answer Book, I have put a response by our friends in Canada—Incut. There is a lot of detail about different types of syncrudes and the product properties therein.

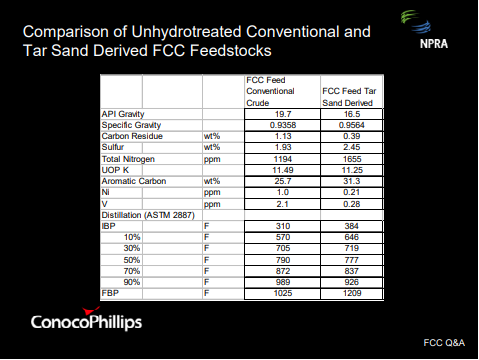

WARDINSKY (ConocoPhillips)

ConocoPhillips is in the process of reconfiguring a couple of our refineries to run large quantities of Canadian tar sand derived feedstocks. This table shows a comparison of feed properties from what the units are currently running and comparing them to some premises that we have for some tar sand derived materials. As you can see, the tar sand derived feedstock is heavier. It contains higher levels of sulfur and nitrogen. It is more aromatic but does not contain as much carbon residue as the conventional crude. The more aromatic nature of the tar sand feedstock is indicated by the comparison of the UOP K factors. The tar sand material does have a higher nitrogen content as well, and the combination with the higher aromaticity should result in a decrease in conversion across the FCC with increased yields of LCO and decant relative to the yields obtained from the conventional feedstock.

KEVIN PROOPS (Solomon Associates)

I believe that this question asks about opportunity crudes. That means people want to make money on this kind of feedstock. I would like to point out that recently, one of the real opportunities is this kind of natural gas. What we saw with our 2006 field study results was that while some of these refiners were experiencing crude advantages versus the Gulf Coast, perhaps, of a few dollars per barrel, natural gas in 2006 was two-thirds the cost of West Texas Intermediate crude on an FLE basis whereas from 1998 to 2004, it averaged about 94% of WTI price. So the money that could be made in 2006 with opportunity high carbon crudes was as much as pumping in hydrogen that came from natural gas as it was in buying those crudes in the first place. I am going to suggest that even though I do not have a crystal ball and I cannot tell you that the natural gas price will remain this time, those refiners that recently could put the hydrogen back into the gas oil probably made the money running these crudes. The FCC obviously is a carbon-hydrogen balance unit. You can reject some carbon with coke; but if you put a hydrogen-deficient feedstock in, you are going to get hydrogen-deficient products back out again. That is hard to get around by most people. I am advocating that if you are going to hydrotreat anyway, when you go to these kinds of feedstocks, the value is probably to get more hydrogen into the gas oil.

RON BUTTERFIELD (Intercat)

We have a northeast refiner who runs predominantly Canadian syncrude and they have been using bottoms cracking additives since mid-2001. It helps to control their bottoms yield. Also, they found that bottoms cracking additive helps to precrack the heavy components at a lower coke yield so they can control a lower temperature in the regenerator.